The GFC of 2008, triggered by the illegal leveraging of the US housing market, saw the reserves of countries drained around the globe. The next […]

Search Results for: bail in

A Crisis Worse Than ISIS? Bail-Ins Begin

While the mainstream media focus on ISIS extremists, a threat that has gone virtually unreported is that your life savings could be wiped out in […]

Secret of Iceland economic miracle: Jail bankers, let banks go bust & no bail-out

I encourage you to watch this video, to understand how the Icelanders rapidly recovered from the 2008 crisis. Except there’s one core element not discussed. […]

The Ebola Epidemic Silver-Lining: IMF Bailouts For Everyone

Here is an interesting take on the Ebola Epidemic. It’s always good advice to follow the money…

Treasury still working on Australian ‘bail-in’ law

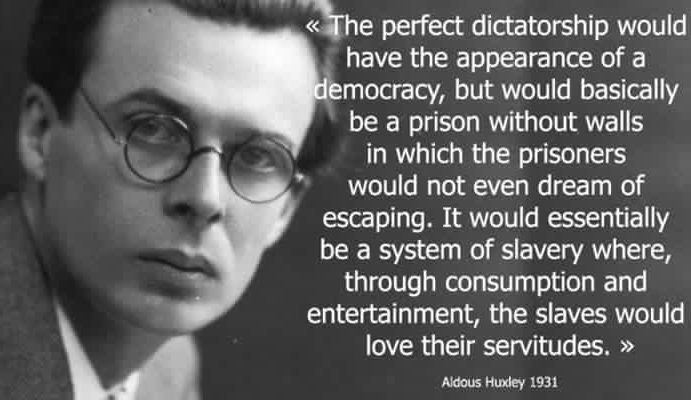

Thank you, John. For me, the connection to the confiscation of depositor’s funds in Cyprus is the key. In line with David Icke’s “Totalitarian Tiptoe” […]

The War On Paper Currency Begins: ECB Votes To “Scrap” 500 Euro Bill

Update: in case there was any doubt about the ECB’s true intentions, we just got the official “denial”: DRAGHI: ANY ECB ACTION ON EU500 NOTE […]

The Big Short is a timely warning for 2016

The recently released movie “The Big Short” came highly recommended from several sources, so I was keen to view it – and it did not […]

When you Deposit Funds in a Bank, it Becomes “Their Money”

Although there has been quite a bit said and written about this recently, I felt it important enough to revisit, as I don’t believe the […]

Kim Dotcom planning a crowdfunded, secure Internet replacement – Meganet

Kim Dotcom is a highly intelligent, practical Internet entrepreneur that the MPAA had the US Government target some 3 years ago, breaking many laws in […]

“Let Me Explain What Happens Next…” – A Reader Sums It All Up Very Ominously

I quote this article from Zero Hedge: A reader recently wrote me a long letter on how he feels about all this ‘Plandemic’ stuff. I […]

Recent Comments